Urban solar energy expanded rapidly as solar modules became cheaper. But rising panel prices could reshape how cities deploy solar power in cities and plan future energy systems.

For more than a decade, the global energy transition has enjoyed a remarkable driver: solar modules kept getting cheaper. According to the International Energy Agency (IEA), the cost of solar photovoltaic (PV) modules fell by more than 80% over the past decade, helping solar become the fastest-growing source of electricity worldwide. This dramatic cost decline has been one of the key forces enabling the rapid expansion of urban solar energy around the world.

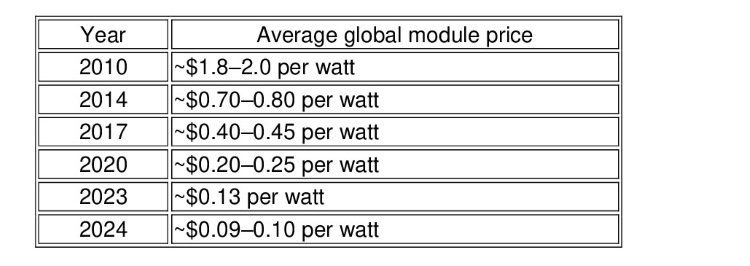

Table 1. The dramatic fall in solar module prices over the past decade

Sources: IRENA, BloombergNEF, global PV market data.

Recent market reports indicate that module prices reached record lows of about $0.096/W in 2024, reflecting intense competition and manufacturing overcapacity. For cities, this price collapse was transformative. Falling module costs made rooftop solar and distributed energy projects financially viable for schools, housing developments, and municipal infrastructure. That era may be entering a new phase.

Industry experts now warn that prices for solar modules could rise by 20–30% by 2026. Solar power will remain one of the most competitive energy sources, but this shift signals a structural change that carries direct implications for city planners, developers, and policymakers working on urban solar energy strategies.

Why prices are rising

1. A shift in fiscal policy

Starting April 1, 2026, China is expected to eliminate the 9% VAT export rebate previously applied to solar module exports. For manufacturers, this effectively reduces export incentives and is widely expected to feed directly into higher export prices. Industry commentary and statements from the China Photovoltaic Industry Association (CPIA) confirm this adjustment as part of broader efforts to stabilize prices and curtail unproductive competition.

2. Materials cost pressures

Silver is a key input in photovoltaic cell manufacturing. The global expansion of solar deployment has significantly increased industrial demand for silver, which is used for electrical contacts in PV cells. Analysts expect demand for silver from solar manufacturers to grow dramatically in the coming decade, putting upward pressure on production costs

3. Market maturity and consolidation

After years of capacity expansion and aggressive price competition, authorities and industry bodies in China are encouraging the retirement of inefficient production lines and promoting consolidation. This is shifting the market away from margin-pressured pricing toward a more balanced industry structure.

Together, these factors suggest that the era of consistently falling solar prices may be giving way to a period of price rebalancing rather than sharp decline.

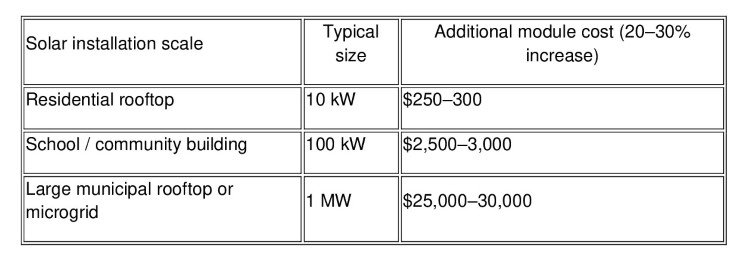

What a 20–30% increase means for cities

Average module prices are currently around $0.13 per watt. A 20–30% increase would push prices toward roughly $0.16–0.17 per watt. To many observers, that looks modest. However at city scale the impact becomes meaningful. Once applied to municipal-scale projects (schools, public buildings, or urban microgrids) the additional costs quickly accumulate, affecting investment decisions in solar power in cities.

Table 2. What a 20–30% increase in solar module prices means at different scales

Source: BloombergNEF PV market data; author calculations.

For municipal budgets and financing models built around tight payback periods, these changes are significant. Cities in Europe, North America, and Asia are increasingly integrating solar into climate action strategies — not only for decarbonization but also for resilience, energy cost stability, and local economic development through urban renewable energy systems.

According to the IEA’s Renewables 2023 report, distributed solar, including rooftop and urban applications, is expected to play a central role in the expansion of renewable electricity worldwide and particularly in the growth of distributed solar in cities.

Several major urban programs illustrate the scale of municipal solar deployment.

In Paris, for example, the city government has expanded rooftop solar installations on municipal buildings as part of its Climate Action Plan, strengthening the role of urban solar energy in the city’s energy transition. Schools, sports facilities, and public administrative buildings are gradually being equipped with photovoltaic systems in order to increase local renewable generation and reduce dependence on external energy supply.

In New York City, the Solarize NYC initiative and community solar programs have encouraged thousands of households and small businesses to install rooftop systems. By simplifying permitting procedures and offering financial incentives, the city has significantly accelerated distributed solar adoption.

Programs like these depend heavily on predictable equipment costs. Even relatively modest increases in module prices can alter the financial assumptions behind municipal procurement programs or slow the expansion of large rooftop initiatives supporting urban solar energy deployment.

A temporary shock or a new normal?

Most analysts expect the coming months to produce cyclical market effects. In the months before April 2026, demand may spike as buyers attempt to secure modules under the current export rebate structure. Some forecasts suggest mid-2026 could represent a peak pricing period. By late 2026, as supply adjusts and demand stabilizes, module prices may moderate again.

However, the deeper market dynamics appear to be shifting. The solar industry is entering a more mature phase characterized by normalized margins, reduced overcapacity, and greater geographic diversification of manufacturing.

Trade policy is also becoming a stronger influence on the sector. The United States has already announced plans to increase tariffs on certain imported solar products, with some duties potentially reaching 50 percent. Similar protectionist measures are emerging in other regions as governments attempt to secure domestic supply chains.

These policy shifts are already influencing corporate strategy. Leading manufacturers such as Longi and Jinko Solar are investing in production capacity in Southeast Asia and North America in order to reduce exposure to tariffs, geopolitical risks, and supply-chain disruptions.

What this means for urban solar energy planning

Solar remains one of the most competitive energy sources. But the era of continuously falling prices may be coming to an end. For cities, this shift has strategic implications.

Photo: Freepick

Many municipal climate plans were built on the assumption that solar costs would continue to decline year after year. With price trajectories becoming less predictable, urban planners and energy departments may need to adjust their strategies.

Possible responses include:

- adopting more flexible budgeting for solar deployment programs

- implementing phased procurement rather than single large purchases

- diversifying supply chains to reduce tariff and logistics risks

- integrating solar into broader distributed energy and resilience strategies.

Rising material costs may also accelerate technological innovation. Research into copper-based photovoltaic cell technologies, for example, aims to reduce dependence on silver and stabilize long-term manufacturing costs.

A market growing up

The age of ultra-cheap solar may be fading. What is emerging instead is a phase in which solar power is valued not only for cost competitiveness but also for resilience, diversification, and strategic deployment, particularly within urban energy systems.

A recent analysis by Boston Consulting Group argues that the next phase of the renewable energy transition will be defined less by falling generation costs and more by system flexibility – the ability to integrate variable renewable energy sources, balance demand and supply, and manage distributed energy networks.

Cities will play a central role in this transformation. Urban energy systems increasingly combine rooftop solar, battery storage, electric mobility, and digitally managed grids. In such environments, flexibility becomes as important as generation capacity, especially as distributed solar in cities continues to expand.

Recent geopolitical developments also highlight the importance of energy resilience. Escalating tensions in the Middle East and the conflict involving Iran have contributed to renewed volatility in global oil and gas markets, pushing energy security back to the forefront of policy debates.

In this context, locally generated renewable energy, including urban solar energy, becomes not only a climate solution but also a strategic asset.

Solar power may no longer be getting dramatically cheaper every year. But its strategic importance for cities is only growing. The next stage of the energy transition will depend less on falling prices and more on how effectively cities integrate renewable energy into urban infrastructure, planning, and resilience strategies.

Authors: Daniel Fisher and Elena Meleshkina