As Southeast Europe accelerates the deployment of renewable energy, battery storage is rapidly becoming one of the region’s most important infrastructure and investment questions. Across the Balkans, growing solar and wind capacity is beginning to expose structural challenges related to grid flexibility, energy pricing, and long-term project bankability.

Ahead of Balkan Battery Day 2026, New Polis spoke with Alex Blomfield, Partner at Clyde & Co, about the evolving energy storage market in Southeast Europe, the regulatory and financing challenges facing battery projects, and why the Balkans are increasingly attracting international investor attention.

From traditional energy to storage

You have worked on energy and infrastructure projects across more than 70 countries, advising investors, governments, and developers. What initially drew you to the energy sector, and how has your focus evolved with the rapid growth of renewables and energy storage?

I started working in energy with a secondment to BP’s Australasian headquarters in Melbourne as a young lawyer in 2005. I then moved to London to become a projects and project finance lawyer in 2006. In this role I started off with a broad energy and infrastructure focus. Over time I have had the privilege to be able to specialise in renewables and energy storage. Making a tangible contribution to the energy transition and the mitigation of climate change is a key motivation for me working in the sector.

Balkan Battery Day

Balkan Battery Day 2026 will bring together key players in the region’s storage market. In your view, what makes this event particularly timely for the Balkans today?

The timing is perfect in my view. The Balkans are entering a phase where rapid renewable energy deployment in solar and wind is beginning to expose structural gaps in grid flexibility. We have already experienced this phase in NW Europe and the Nordics, with negative pricing and reduced capture rates from existing renewable assets. The same is gradually being felt across CEE, where Clyde & Co already supports the rollout of storage projects. Battery storage has moved from a conceptual solution to a practical necessity, both from a grid and an investment returns perspective.

At the same time, investor interest in the region is increasing, often driven by eastwards expansion of existing European portfolios. There remains a clear need for bankable frameworks and precedent transactions to be developed in the Balkans. Against the backdrop of broader European energy supply and security discussions after recent Middle East conflicts and the continent’s decarbonisation objectives, this creates both urgency and opportunity for the market.

The event focuses on real projects and active market participants. What kinds of conversations or outcomes do you expect it to generate, beyond traditional networking?

I would like the event to be focused on shared experiences in the BESS markets, to move beyond high-level dialogue and toward more practical outcomes. Discussions should centre on developing the options for bankable revenue models for storage, including tolling structures, optimisation agreements, capacity-style mechanisms, and hybrid arrangements.

There should also be meaningful engagement on how risk is allocated across developers, lenders and offtakers, as well as steps toward greater contractual standardisation. The industry also needs more experience-sharing around risk allocation and transaction structuring to help reduce the time to financial close and ease transactional friction. Reducing the time to reach financial close and easing transactional friction are key elements to get the market moving. Ultimately, events of this nature can serve as a catalyst for early-stage deal origination and the formation of strategic partnerships.

From your perspective, what differentiates Balkan Battery Day from other energy or renewables events in the Balkans?

What stands out is the clear emphasis on execution. The event prioritises live transactions, real assets and active market participants. It also benefits from a regional focus, addressing the specific challenges and opportunities of Balkan markets rather than applying a broad pan-European lens. This combination of commercial focus and regional specificity should make the dialogue more practical and actionable.

Energy storage, pressure on the grid and new investment opportunities

Energy storage is moving rapidly up the agenda across Europe. From your experience, what is driving this shift in the Balkans?

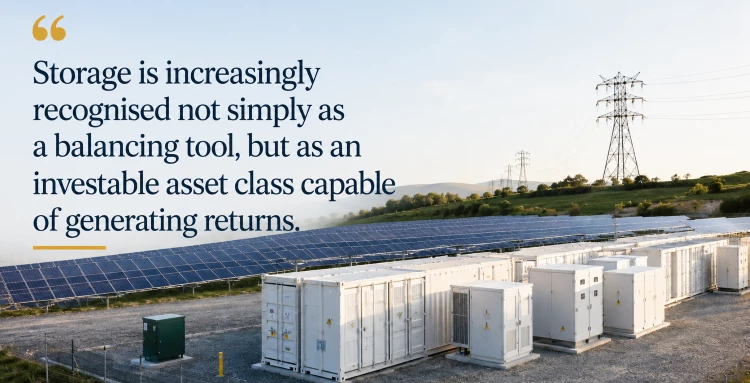

With the growth of renewables in the Balkans, the region is not immune from solar cannibalisation and negative price hours, which render the economics of solar projects increasingly challenging. In addition, from a grid management perspective the increased penetration of intermittent renewable generation is introducing volatility into local power markets and placing strain on existing grid infrastructure. Storage is increasingly recognised not simply as a balancing tool, but as an investable asset class capable of generating returns. In parallel, international investors are looking toward the Balkans as a higher-yield alternative to more saturated Western European markets, further accelerating momentum.

From a project and financing perspective, where do you currently see the most activity in energy storage across the region? Are there particular markets or project types gaining traction?

Activity is currently most pronounced in relatively advanced markets such as Romania, Greece and Bulgaria, where regulatory developments and access to EU funding mechanisms are supporting project viability. In Greece, the country is moving beyond subsidies for BESS and towards merchant-ready territory, with its new BESS Priority Regime incentivising standalone non-subsidised BESS projects via fast-tracked grid connections. In Bulgaria the National Renewable Energy Storage Infrastructure Program provided capital grants to almost 14 GWh of storage in two rounds in 2025.

Romania is catching up: It announced an intention last year to subsidise the installation of at least 2000 MWh of standalone energy storage facilities and recently received approval from the European Commission to implement the scheme.

There is also growing interest in co-located solar and storage projects, particularly where grid connection constraints exist. While standalone storage is emerging, much of the near-term pipeline continues to rely on hybrid or partially contracted revenue structures to support financing.

Regulation, bankability and market risk

From a legal and financing perspective, what are the main regulatory or contractual challenges facing energy storage projects in the Balkans today?

The key challenge remains the absence of stable and transparent revenue frameworks. Many markets lack mature capacity or ancillary service mechanisms capable of underpinning long-term cash flows. In addition, there is limited standardisation of storage-specific contracts, which can complicate negotiations and increase transaction costs. Permitting processes and grid connection regimes can also lack consistency and predictability, ultimately impacting bankability.

This being said, experience is growing rapidly, especially in the more advanced markets in the region mentioned already. Regional energy traders and route to market providers are skilling up and offering optimisation contracts for BESS assets, while power purchase agreement buyers are looking for integrated BESS and renewable generation projects.

In particular PPA buyers are interested in benefits co-located BESS can provide. The key now is to find a suitable arrangement that supports the required capital expenditure such as a price floor from an offtaker. This can facilitate project financing by providing more revenue certainty.

How do differences in national regulatory frameworks across the region affect investment decisions and cross-border energy projects?

Regulatory fragmentation is a significant constraint. Divergent frameworks across neighbouring jurisdictions increase complexity and reduce the ability to scale investments on a regional basis. They also complicate cross-border trading and optimisation strategies, which are particularly relevant for storage assets. As a result, investors tend to prioritise markets where regulatory regimes are clearer, more stable and better aligned with European standards. However, the Clyde & Co team has experience handling these types of complexities and can act as a trusted advisor to investors and other market participants seeking to navigate these risks.

What changes in policy or market design would be most important to unlock further investment in storage and renewable energy in Southeast Europe?

The most impactful change would be the introduction of clear, investable revenue mechanisms—whether through capacity markets, long-term contracts or other forms of revenue stabilisation. In parallel, it is important to establish a clear legal classification for storage as a distinct asset class. Improvements in grid access processes and greater alignment with EU market design principles would also be critical in attracting sustained international investment.

The next phase of the Balkan energy market

Looking ahead, what do you see as the biggest opportunity and the biggest risk for the energy storage market in the Balkans over the next five to ten years?

The opportunity is substantial. Storage has the potential to become a core infrastructure component underpinning the region’s energy transition, with the Balkans positioned as a high-growth market offering attractive returns. Increasing integration with wider European energy markets should further enhance liquidity and value creation.

However, the risks should not be underestimated. There is a real danger of over-reliance on uncertain revenue forecasts, which could lead to mispricing and subsequent valuation corrections. Regulatory inconsistency remains a key concern, as does the potential for revenue compression as markets mature. Ensuring that investment frameworks are grounded in realistic assumptions and supported by robust contractual structures will be essential to avoid repeating the challenges seen in earlier renewable cycles. Nevertheless, demand for BESS projects across the Balkans continues to grow, creating significant opportunities for investors despite the risks associated with a still-evolving regulatory environment.

Read and watch more interviews here